The average cost of a house solar PV and battery storage system is expected to reach ‘socket parity’ next year according to Bloomberg New Energy Finance. This means that the cost to consumers of the energy produced by their solar and battery system is the same amount per kWh as the energy accessed from the grid. This coincides with the prevalence of behind the meter residential batteries growing due to the costs of battery technology declining, favourable consumer sentiment and the introduction of government subsidy schemes.

This year, in addition to our assessment of the state of retail competition, the Commission conducted research into behind the meter battery technology and related services. Our objective in undertaking the study was to assess whether retail energy competition is promoting innovation in behind the meter battery products and services.

We found that the retail electricity market is reacting to batteries much earlier and in a more way sophisticated than it did with residential solar PV. Despite battery technology being in the early phase of development, our analysis indicates that competitive retail electricity markets are facilitating innovation and providing electricity offers targeted to the wants and needs of individual consumers.

Our approach to this research is divided into three sections:

- context

- current battery related products and business models

- assessment of the business models.

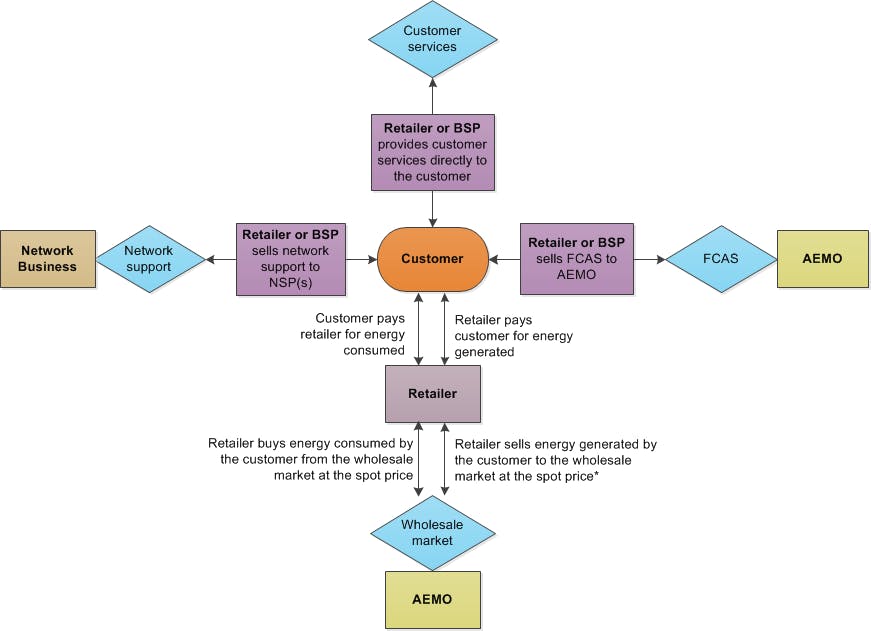

Before we could assess whether retail market competition is facilitating innovation we needed to outline how behind the meter battery products, and the functions they can provide, fit within the existing market design. In doing so, we identified a new business type that has emerged in the retail market – what we have called the ‘battery service provider’ (BSP). The BSP controls behind the meter batteries and may come in many forms. A BSP aggregates battery storage units, and potentially other types of distributed energy resources (DER), into a virtual power plant (VPP).

Battery storage devices have a range of technical capabilities, including the provision of energy, voltage control, frequency regulation and reactive power. These capabilities can be used to provide a range of services that are of value to a number of parties, including consumers, retailers, network businesses and the system operator the Australian Energy Market Operator (AEMO). We set out these capabilities and who can realise their value under the existing market design below.

Existing market design — Access to value streams

Our research mapped out the current ways consumers are provided with battery technology and related services. The results found the potential for residential battery storage in Australia was creating a new type of energy entrepreneur. These businesses are working with global battery providers, such as Tesla and Sonnen, to combine their batteries to form VPPs.

From this we found that there are three main business models — which describe the commercial relationship between retailers, BSPs and consumers —supplying residential customers with battery related products and services. These business models are:

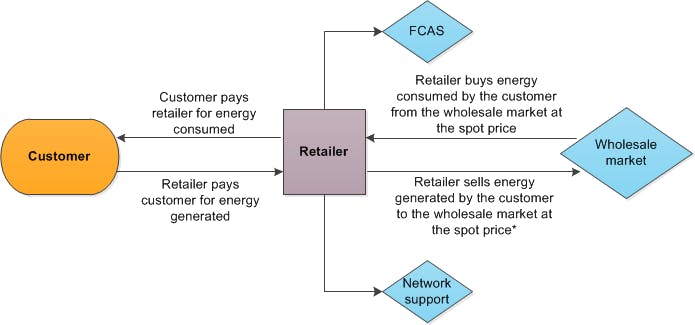

- Retailer led — in this business model the customer only interacts with their electricity retailer. The retailer coordinates the sale, installation, operation, and maintenance of the battery for the customer. The retailer realises the benefits, and pays the costs, of the battery's operation to realise the various value streams. An example of this model is AGL's VPP in South Australia.

Business model 1 – Retailer-led

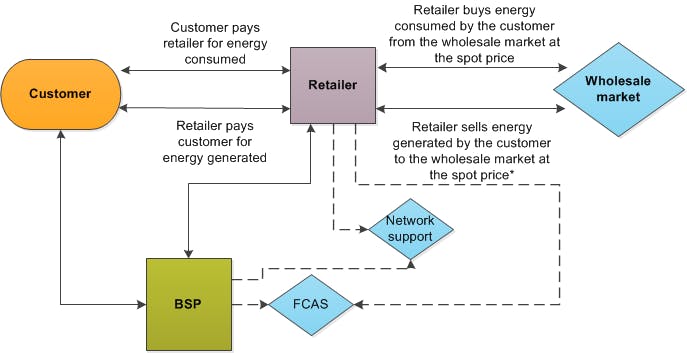

- Retailer and BSP coordination — in this business model a BSP and a retailer develop joint product offerings for customers. Typically, this involves the BSP selling, installing and operating the battery for the customer. The retailer then makes specific retail market offer(s) with the BSP to the customer. Examples of this model are Reposit Power and Powershop, and Sonnen and Energy Locals.

Business model 2 – Retailer/BSP coordination

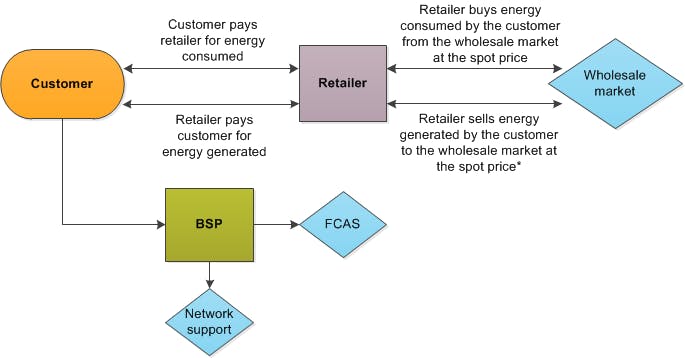

- Passive retailer-BSP led — this model involves no active participation or coordination from the retailer. The customer has a standard relationship with the retailer and has a separate relationship with a BSP that operates and provides value from their battery. An example of this model's passive retailer is Amber Electric.

Business model 3 – BSP led

Using the above three business models we next assessed whether retail energy competition is promoting innovation related to battery technology products and services. To do this we looked at criteria from both the consumer and retailer point of view. Our analysis reveals that while all models have their benefits and drawbacks, activity under these frameworks indicates that competitive retail markets are facilitating innovation and are likely to result in electricity offers that meet consumers’ preferences.

Of note is the wide variety of retailer sizes, strategies and skills within the national electricity market (NEM) that facilitate innovation in the behind the meter battery storage space. The analysis also demonstrates that there is not one clearly superior business mode. Over time, competition will reveal which business model(s) consumers prefer, with those that do not meet consumers’ preferences likely to fall away.

For stakeholders interested in more detail on this research, our full assessment is outlined in Chapter 8 of the Final report.

We also note that we plan to complete similar analysis and assessment of innovation in the retail energy market in relation to electric vehicles in our 2020 review of retail energy competition.